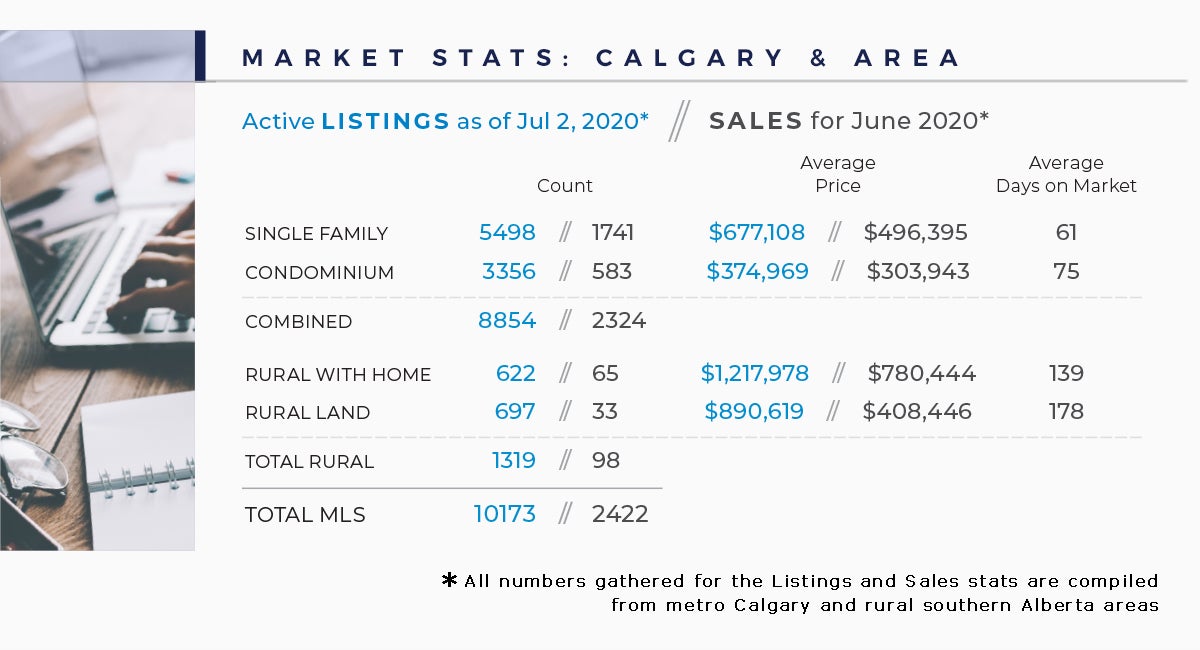

After three months where COVID-19 weighed heavily on the housing market, sales activity in June continued to trend up from the previous month, totalling 1,747 units.

Caution remains necessary, as monthly sales are nearly two per cent lower than activity recorded last year. However, this represents a significant improvement compared to the past several months, where year-over-year declines exceeded 40 per cent.

“Recent price declines, easing mortgage rates and early easing of social restrictions are likely contributing to the better-than-expected sales this month,” said CREB® chief economist Ann-Marie Lurie.

“However, the market remains far from normal. Challenges, such as double-digit unemployment rates, will continue to weigh on the market for months to come.”

New listings in June totalled 3,335 units, a six per cent increase over last year. The recent rise in new listings caused inventories to trend up, but they remain well below last year’s levels.

Despite some recent monthly gains in supply, sales activity was high enough to cause the months of supply to dip below four months for the first time since May 2019. If this trend continues, it should help to ease the downward pressure on prices.

Residential benchmark prices are comparable to last month, but they remain nearly three per cent lower than last year’s levels.

HOUSING MARKET FACTS

Detached

Sales activity in June totalled 1,092 units. This is an improvement over the past few months and only slightly lower than last year’s levels.

Despite citywide declines, year-over-year sales activity improved in the City Centre, North East, North, South East and East districts.

June also saw an increase in new listings, which is causing some monthly gains in inventory. However, increased sales offset the rise in new listings, causing the months of supply to trend toward more balanced conditions.

Detached benchmark prices remained relatively stable compared to last month but were two per cent lower than last year’s levels. Year-over-year price declines were recorded across most districts, with the largest declines in the North West, North East and City Centre districts.

Apartment

Apartment sales totalled 227 units in June. This is an improvement from the 136 units last month, but it is still nearly 13 per cent lower than last year’s levels and over 30 per cent lower than longer-term averages.

New listings rose compared to last month and last year. This did translate into some monthly inventory gains, but overall inventory levels remain lower than last year’s levels.

The months of supply has come down from the high levels recorded over the past few months.

Benchmark prices continued to trend down this month, totalling $240,900. This is a year-over-year decline of nearly four per cent.

The resale apartment sector continues to be one of the hardest hit in terms of relative declines in both sales and prices.

Attached

The attached sector has faced the smallest impact from the pandemic. June sales were nearly three per cent higher than last year’s levels and remain comparable to longer-term averages. The attached sector has generally benefited from its status as a more affordable alternative to the detached sector.

Like the detached sector, the attached sector saw new listings rise compared to both last year and last month. However, the months of supply trended toward more balanced conditions and improved over last year’s levels.

Benchmark prices remained relatively stable compared to the previous month, but fell by nearly four per cent compared to last year. The higher price decline in this sector could be a contributing factor to the improving sales activity.

REGIONAL MARKET FACTS

Airdrie

Following declines over the past three months, June sales rose above last year’s levels. While the monthly gain was significant, it was not enough to offset previous pullback, as year-to-date sales remained nearly eight per cent below last year’s levels.

Airdrie also saw new listings rise, but inventory levels remain well below last year’s levels. The months of supply dropped below three months and is lower than pre-COVID-19 levels. If the supply/demand balance stays in this range, we could start to see some of the downward price pressure ease.

Airdrie’s benchmark price was $327,400 in June. This is down compared to the previous month and over two per cent lower than last year’s levels. Year-to-date prices remain just below last year’s levels.

Cochrane

Sales in Cochrane this month improved over last year’s levels. At the same time new listings also rose, causing some growth in inventory levels. However, the improvement in sales outpaced the gains in inventory, causing the months of supply to trend down.

Supply/demand balances are improving, but it takes time before this is reflected in prices. In June, the benchmark price was $394,900. This is slightly lower than last month and nearly four per cent lower than last year. It will likely take several more months of more balanced conditions before seeing any impact on home prices.

Okotoks

June sales remained relatively stable compared to last year’s levels. However, with steep declines in April and May, year-to-date sales remain well below both last year’s levels and longer-term trends.

Recent gains in new listings caused some monthly gains in inventory levels. The monthly gain in inventory was not enough to offset the monthly increase in sales, causing the months of supply to trend down to three months in June.

Benchmark prices were falling prior to the COVID-19 pandemic, but the pace of decline increased during the past several months. In June, benchmark prices remained relatively stable compared to last month, but they remain over four per cent lower than last year’s levels.