City of Calgary, February 1, 2021 –

January sales were the highest they have been for the month since 2014, as housing market momentum from the end of 2020 carried over into the start of 2021.

January sales were the highest they have been for the month since 2014, as housing market momentum from the end of 2020 carried over into the start of 2021.Sales activity improved across all product types and across all price ranges.

“Discount lending rates are exceptionally low, which is likely attracting all types of buyers back into the market,” said CREB® chief economist Ann-Marie Lurie.

“New listings in the market were also slightly higher than what was available over the past two months, which is providing more options to purchasers.”

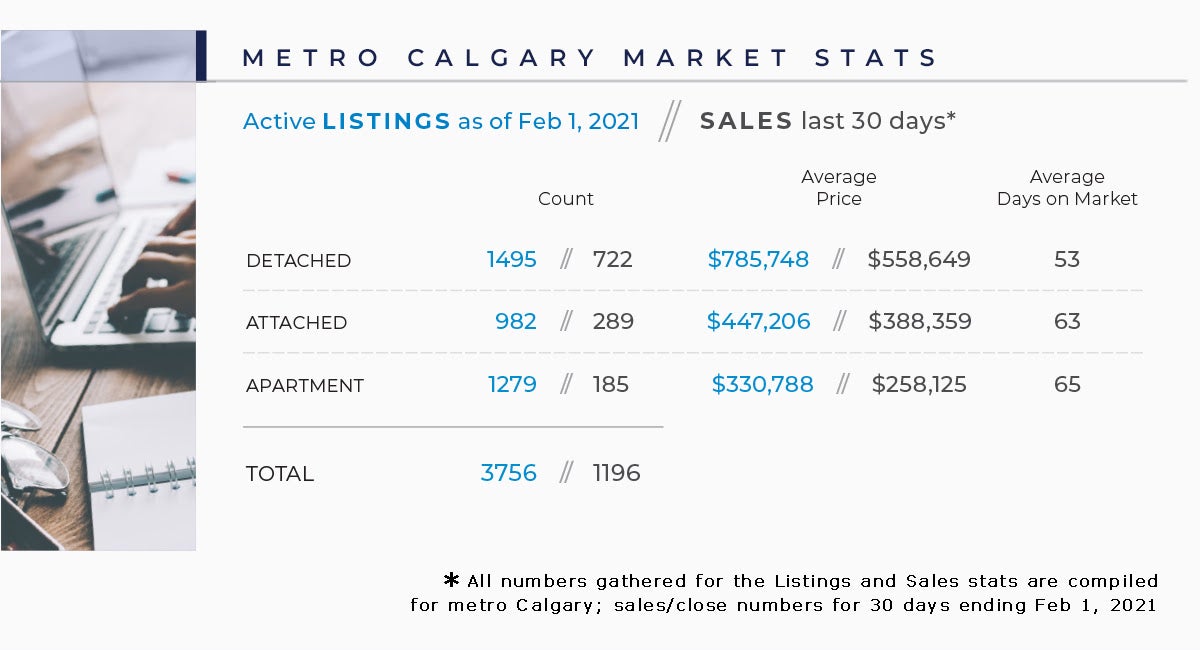

January’s new listings were 2,246 relative to the 1,208 sales in the market, causing inventories to edge up over December levels. These types of movements are typical for January, but 2021 is starting the year with 4,035 units in inventory. This is far lower than the past six years.

Benchmark prices remained at levels relatively consistent with prices recorded at the end of 2020, but they reflect a year-over-year gain just below two per cent.

Average and median prices recorded higher year-over-year gains, likely due to larger gains in sales in the higher end of the market. Those segments do not have the same inventory constraints as lower-priced product.

HOUSING MARKET FACTS

Detached

January sales activity improved across most prices ranges. However, limited inventories for homes priced below $500,000 ensured conditions in those segments remained firmly in sellers’ market territory. This likely prevented stronger sales improvements in this portion of the market.

However, with better supply options at the upper end of the market, sales activity improved.

The citywide months of supply was just over two months, a significant drop from last January where levels were nearly five months. The tighter conditions in this segment supported further gains in prices, which currently sit nearly three per cent above last year’s levels.

Year-over-year price gains range significantly throughout the districts of the city. The largest gains occurred in the North and South East districts. Prices remained relatively unchanged over the previous year in the City Centre and West districts.

Semi-Detached

January sales activity rose over last year’s levels due to gains across most districts. The West end district continues to see slower activity than the previous year.

New listings improved from December levels. This is causing some monthly gains in inventories, but inventory remains well below levels seen last year and the months of supply remained below three months.

Price activity did vary depending on location. Year over year, prices remain over one per cent higher than last year’s levels thanks to strong gains in the North and South East districts. However, persistently high levels of inventory compared to sales contributed to the significant price decline occurring in the West district.

Row

Thanks to gains across nearly every district, sales activity improved compared to the previous year. Unlike the detached and semi-detached sectors, row new listings trended up relative to last month and levels recorded last year.

The rise did result in some monthly gains in inventory levels and caused the months of supply to rise to nearly five months. This is not entirely unusual activity for January. The months of supply remains well below last year’s levels at nearly seven months.

Citywide row pricing remained relatively stable compared to last year and last month. However, there was significant variation depending on location. Year-over-year price gains exceeded four per cent in the City Centre, West and East districts. Meanwhile, prices eased by over three per cent in the North and South East districts.

Apartment Condominium

For the third month in a row, apartment condominium sales rose above levels recorded in the previous year. January levels are the best we have seen since 2014. While new listings have eased compared to last year, they recorded a significant jump over December levels, keeping inventories elevated relative to sales activity.

While prices remain well below previous highs, there were some districts that recorded year-over-year gains. The strongest gains occurred in the North East, East and South districts. However, prices continue to fall in the City Centre, West and South East districts.

REGIONAL MARKET FACTS

Airdrie

Sales activity stayed strong in January. With 103 sales, this was the best January since 2007. New listings improved compared to last month, resulting in some monthly gains in inventory levels. However, the months of supply has remained relatively tight.

With conditions continuing to favour the seller, benchmark prices trended up relative to last month. At $349,100, benchmark prices are over five per cent higher than levels recorded last January. The strongest year-over-year price gains occurred in the detached and semi-detached sectors.

Cochrane

Cochrane sales improved from last January’s levels, but we also saw a notable rise in new listings. This caused the sales-to-new-listings ratio to ease to 63 per cent.

This is a significant improvement over last month, which saw sales levels exceed the level of new listings in the market. Overall, conditions remain relatively tight, with the months of supply staying below three months.

Benchmark prices recorded year-over-year gains across all property types. Overall, benchmark prices remained over four per cent higher than last January’s levels.

Okotoks

After several months of relatively weak new listings, January saw some pickup in new listings relative to the last quarter of 2020.

Sales remained relatively consistent with last year’s levels, causing the months of supply to trend up to three months. This is higher than the extremely tight levels seen at the end of 2020, but it is still significantly lower than the six-plus months recorded in January of last year.

Benchmark prices remained stable compared to last month, but they are over three per cent higher than last January. The gains were driven by the detached sector, as prices continue to ease in the semi-detached, row and apartment sectors.

Click here to view the full City of Calgary monthly stats package.

Click here to view the full Calgary region monthly stats package.